Listen Now

In 2025, pricing became the primary growth lever for industrial companies as volume-driven expansion stalled. Revenue CAGR decelerated to 2.1% post-COVID, yet more than half of industrial firms announced price increases. The results were mixed: firms that acted outperformed peers on revenue and TSR, but many failed to convert those increases into sustained margin expansion. The gap between intent and execution—driven by systemic complexity—remains the defining challenge for industrial pricing organizations.

Pricing as the Strategic North Star

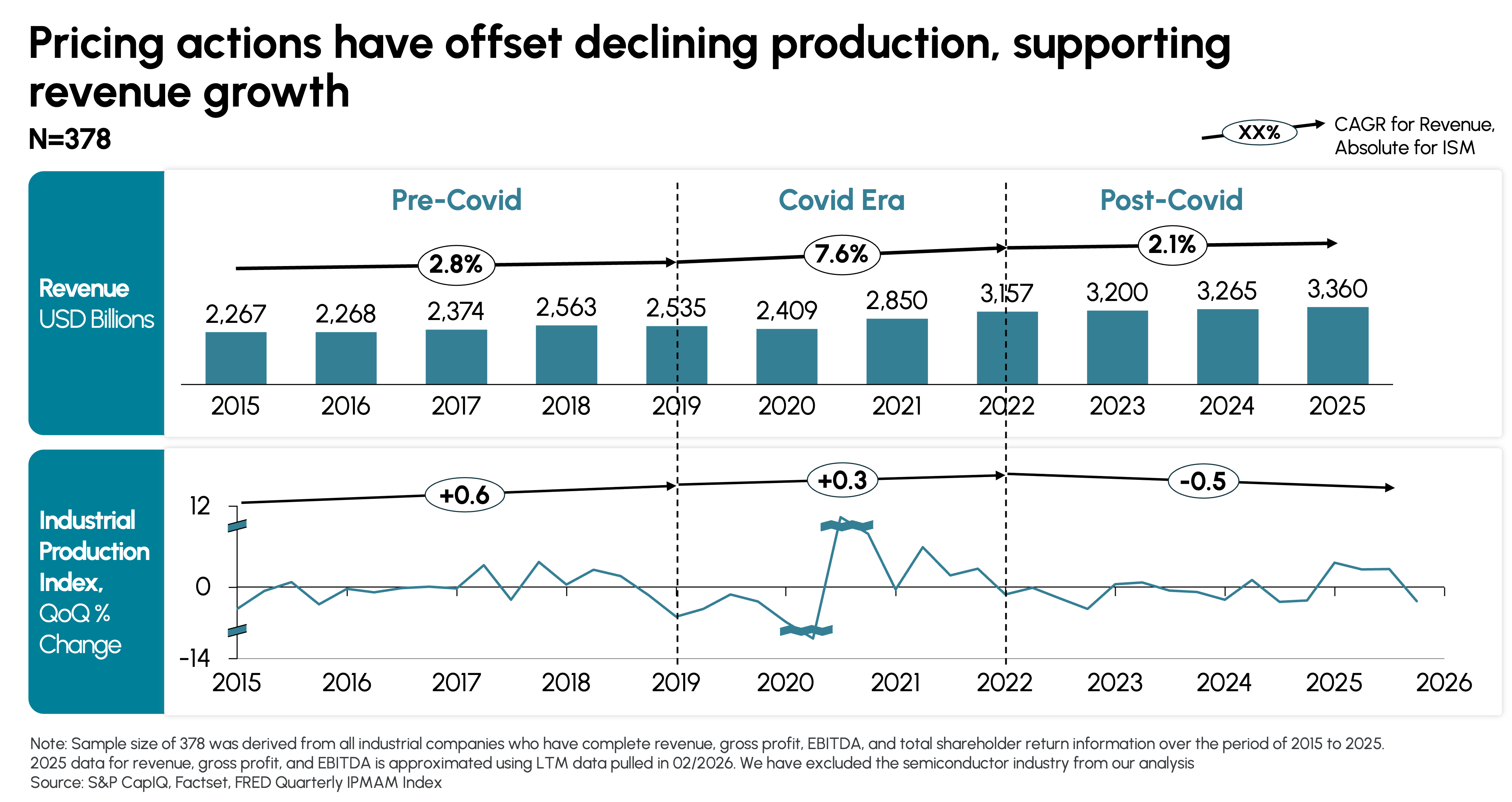

As industrial production declined by 0.5 percentage points post-COVID, companies could no longer rely on volume to drive revenue. Pricing moved from a back-office function to a central pillar of executive strategy. The data is clear: revenue grew from $3,157B to $3,360B between 2022 and 2025 even as production contracted—pricing actions absorbed the shortfall (Exhibit 1).

Exhibit 1

Broad Adoption, Uneven Results

52% of industrial companies announced price increases in 2025, with earnings call discussions on pricing surging 2.5x in H2'25 vs. full-year 2024. Executives across segments were unequivocal on passing on costs as being non-negotiable (Exhibit 2).

Exhibit 2

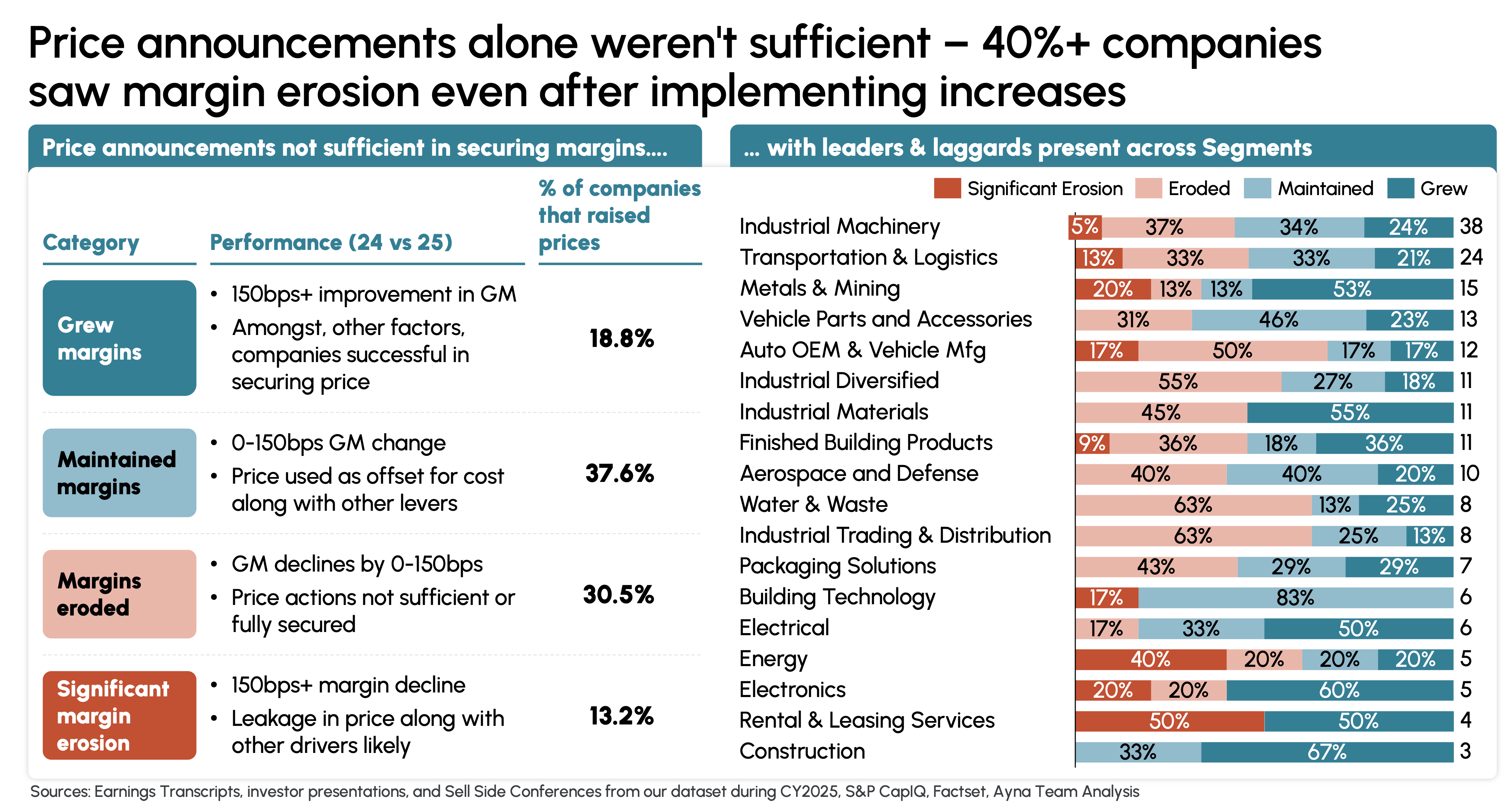

Yet announcing a price increase and realizing it are two very different things. Companies that raised prices outperformed peers by 270 bps in revenue CAGR and 440 bps in TSR—but 43.7% still saw margins contract. Only 18.8% achieved meaningful margin expansion of 150+ bps. The majority merely covered costs or lost ground to leakage (Exhibit 3).

Exhibit 3

Why Execution Fails: The Structural Barriers

Price realization in industrials is undermined by eight systemic barriers. These are not one-off execution failures; they are structural features of the industrial business model that erode pricing gains before they reach the bottom line (Exhibit 3):

- Disjointed Systems: Decades of M&A have created fragmented ERPs and siloed tools—98% of companies cite data quality issues, making real-time margin tracking across thousands of SKUs nearly impossible.

- Complex Portfolios: Industrial companies manage sprawling SKU libraries with thousands of products—many redundant or obsolete. Experts estimate ~60% of parts in a typical portfolio could be rationalized.

- Channel Complexity: Selling through Direct, Distributors, Integrators, Retailers, and eComm creates inconsistent pricing—intermediaries are often incentivized to negotiate prices down even when end-users highly value the product.

- Contractual Rigidity: Multi-year contracts with fixed pricing, price caps, and Most Favored Nation (MFN) clauses delay or dilute pricing actions and limit the ability to pass through cost increases.

- Layered Incentives: Complex rebate and volume discount structures obscure true margin performance, creating silent leakage—in many cases, rebates are paid out even when sales targets are missed.

- Stale Cost Data: Bill of Materials (BOM) cost data is often outdated or incorrect, leaving companies unable to accurately quantify the impact of inflation and tariffs on product-level margins.

- Pricing Inertia: Most industrials default to cost-plus or flat annual price increases rather than value-based models, consistently underpricing engineering reliability and product differentiation.

- Digital Lag: Industrials trail other sectors in CRM, analytics, and pricing tool maturity—creating blind spots on customer price sensitivity and leaving significant margin on the table.

The Path Forward

Pricing maturity is now a structural competitive advantage. The winners in the next industrial cycle will not simply be those that raise prices—they will be those that invest in the data infrastructure, analytics guardrails, and execution discipline to capture and protect them. In a world where volume growth is no longer guaranteed, price realization is the differentiator.