Listen Now

Industrial companies today are operating through epochal change—a level of macro volatility, tariff uncertainty, and technological disruption that is reshaping competitive advantage. At the same time, the sector has never been more essential: industrial firms are building the physical backbone of AI-era data centers and modernizing the power grid. Yet despite this central role, most industrials are struggling with stalled growth, margin pressure, and muted valuations.

Our latest research analyzes how the landscape has shifted—and what distinguishes the companies that are outperforming despite these headwinds. From this, we identify eight core beliefs that define how value will be created in industrials going forward.

Epochal Change In The Business Environment

Industrial companies are navigating a macro environment characterized by uncertainty, historic tariff shocks, and the rise of AI as the economy’s new engine of growth.

Uncertainty in the Macroeconomy

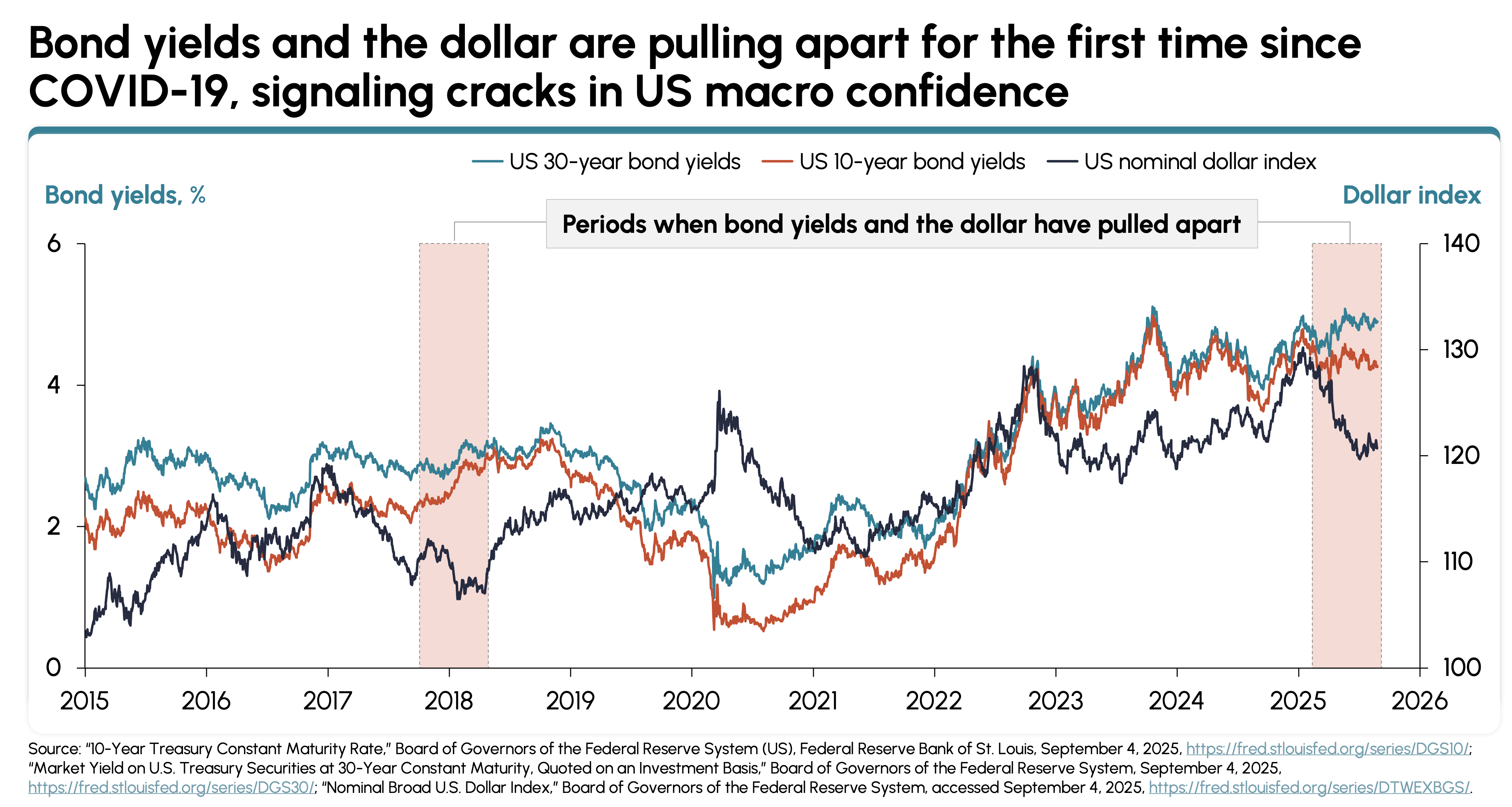

Bond yields and the US dollar diverged for the first time since the pandemic—signaling cracks in macro confidence (Exhibit 1). Emerging markets continue to outgrow advanced economies by more than 200 bps, while industrial and consumer sentiment remain subdued. The ISM Manufacturing Index has stayed in contraction territory for most of 2023–25, and consumer confidence sits below long-term norms.

Exhibit 1

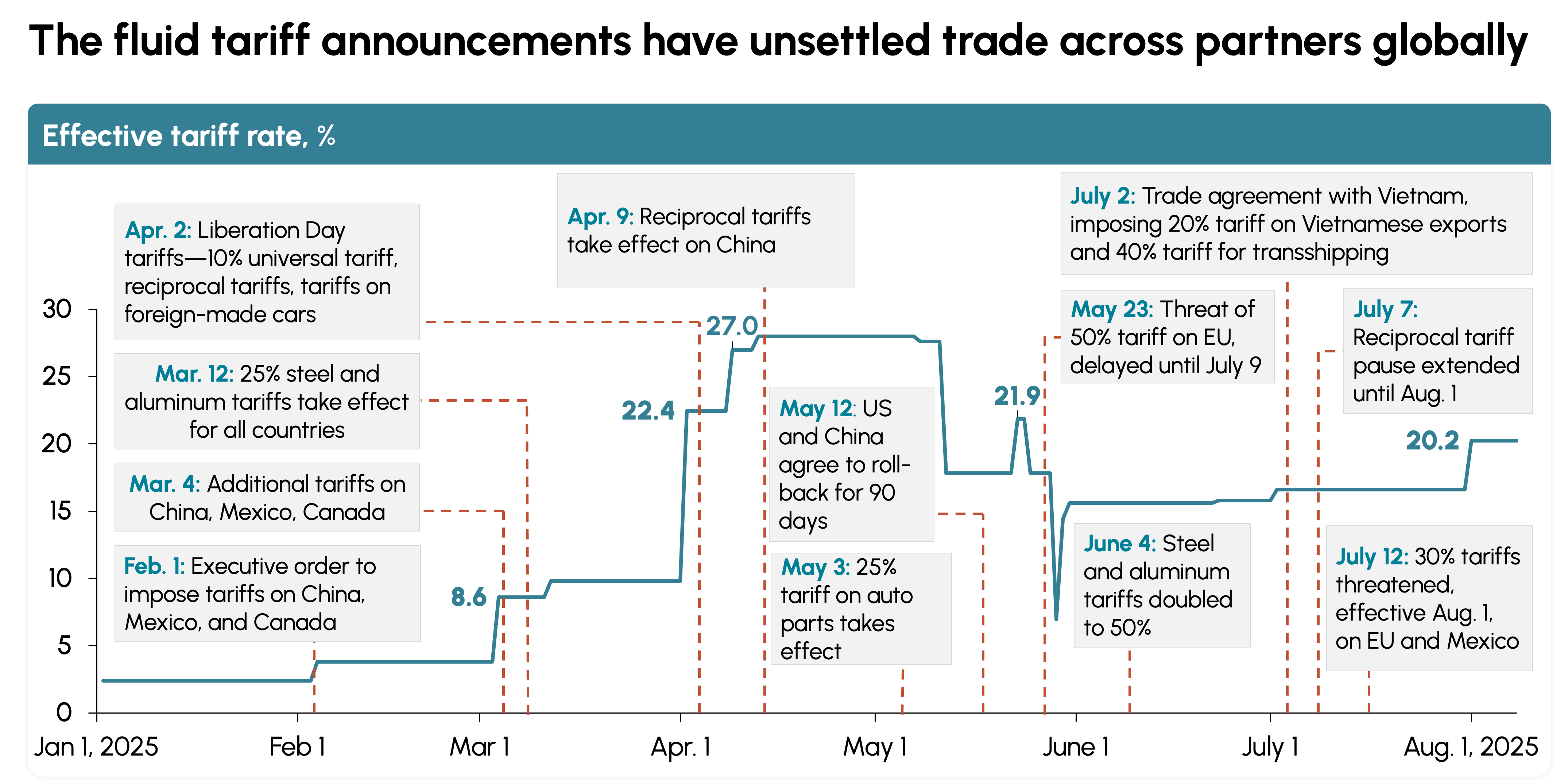

Tariffs Reshaping Trade

The US effective tariff rate surged to its highest level in nearly a century—peaking at 27% in 2025. Tariff measures have been volatile, broad, and increasingly structural (Exhibit 2). Supply chains are being reconfigured as FDI shifts toward Vietnam and Mexico, while price effects are already visible across consumer categories.

Exhibit 2

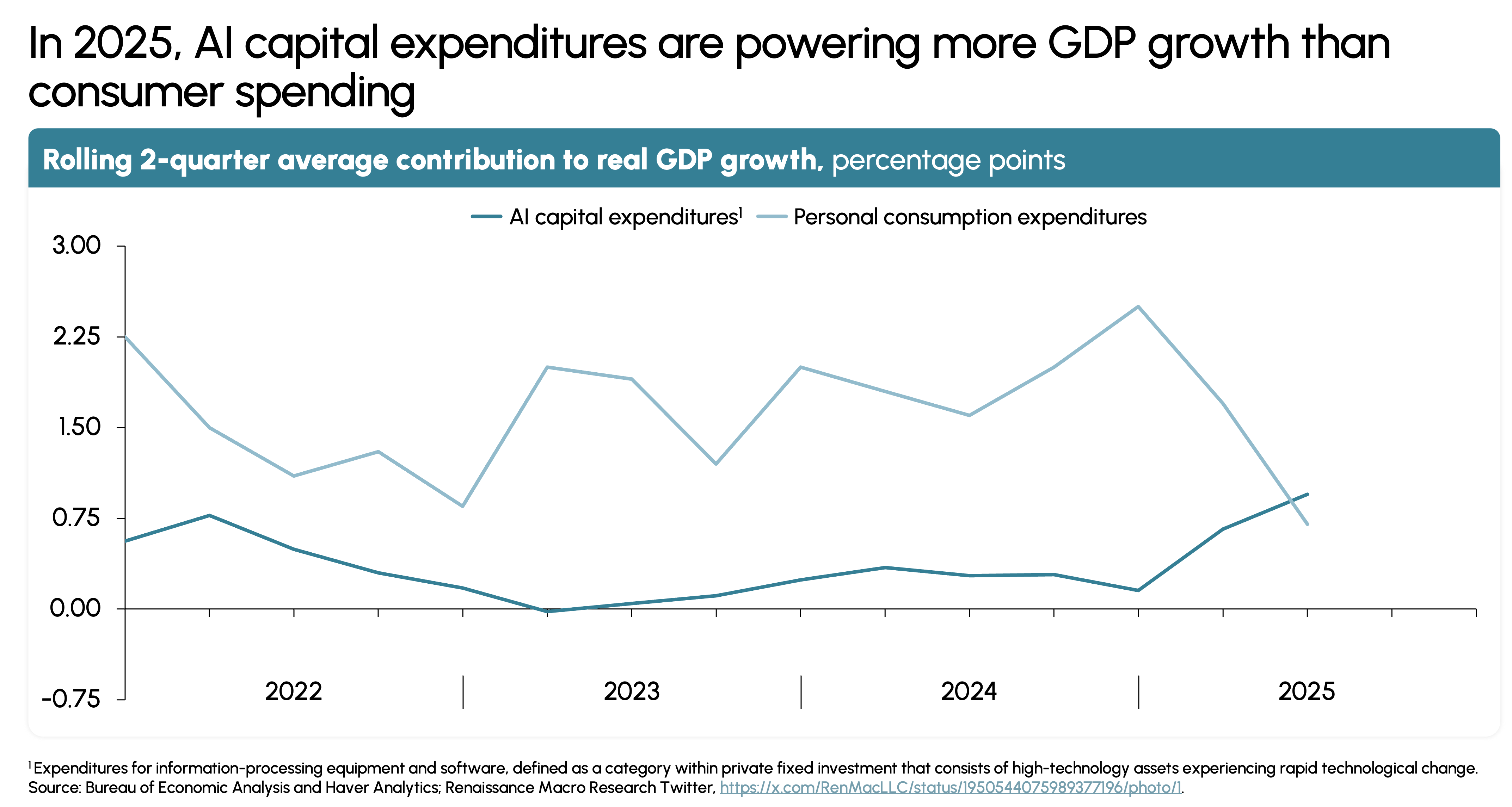

A New Growth Engine: Artificial Intelligence

AI-related capital expenditures now contribute more to GDP growth than consumer spending (Exhibit 3). In 2025, AI CapEx accounted for 0.95% of GDP growth—surpassing personal consumption for the first time. The Mag 7 continue to capture the majority of value, delivering shareholder returns 4× higher than the broader NASDAQ.

Exhibit 3

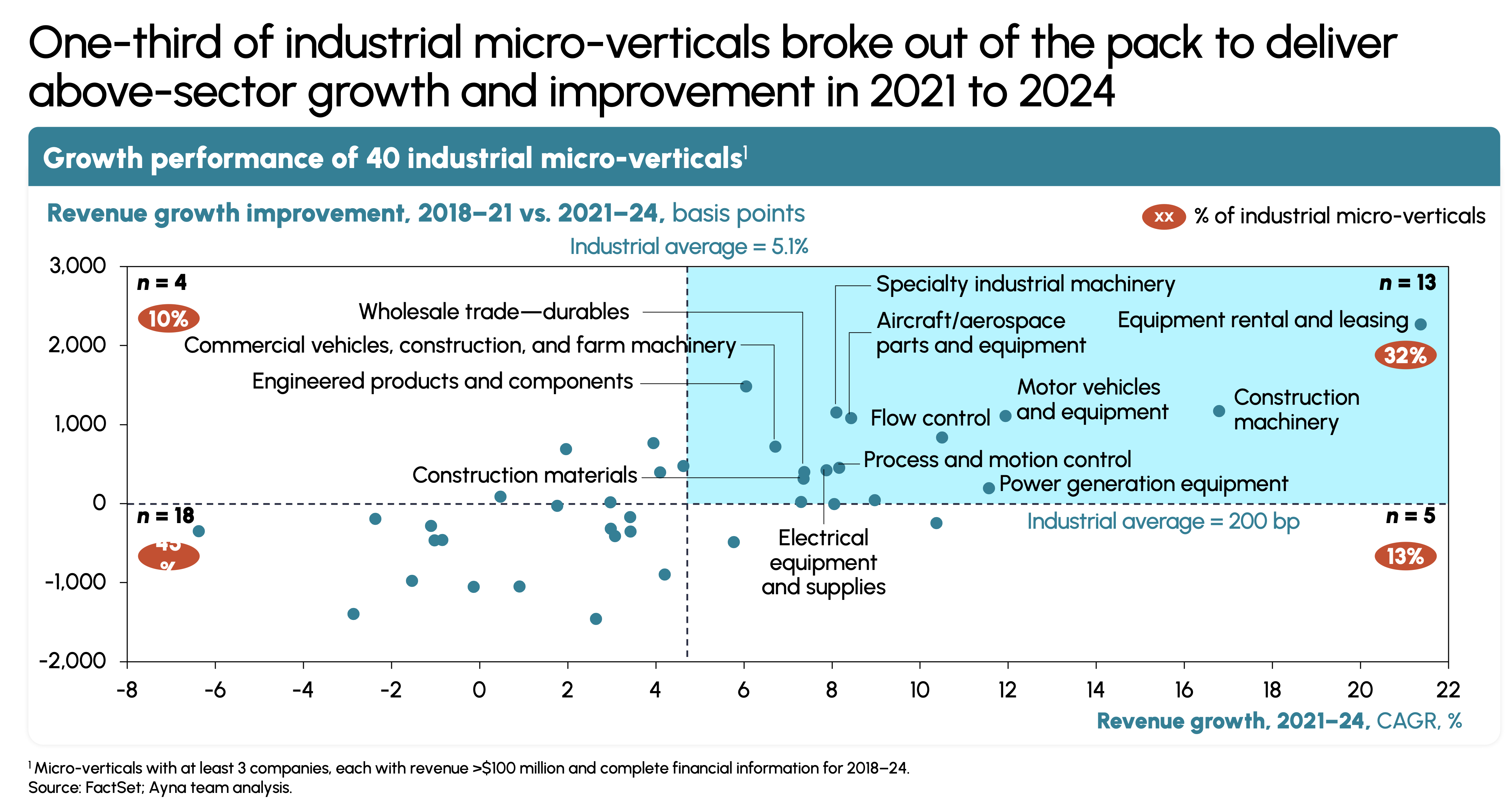

Weak Responses from the Industrial Sector

Sector-wide revenue growth has stalled, leaving industrials among the weakest-performing parts of the US economy for much of the past decade. Yet within this landscape, a subset of micro-verticals is outperforming—particularly those aligned with infrastructure spending, data centers, and electrification. However, a subset of firms broke out of the pack. 32% of micro-verticals showed above-average revenue growth and growth improvement from 2021–24 (Exhibit 4).

Exhibit 4

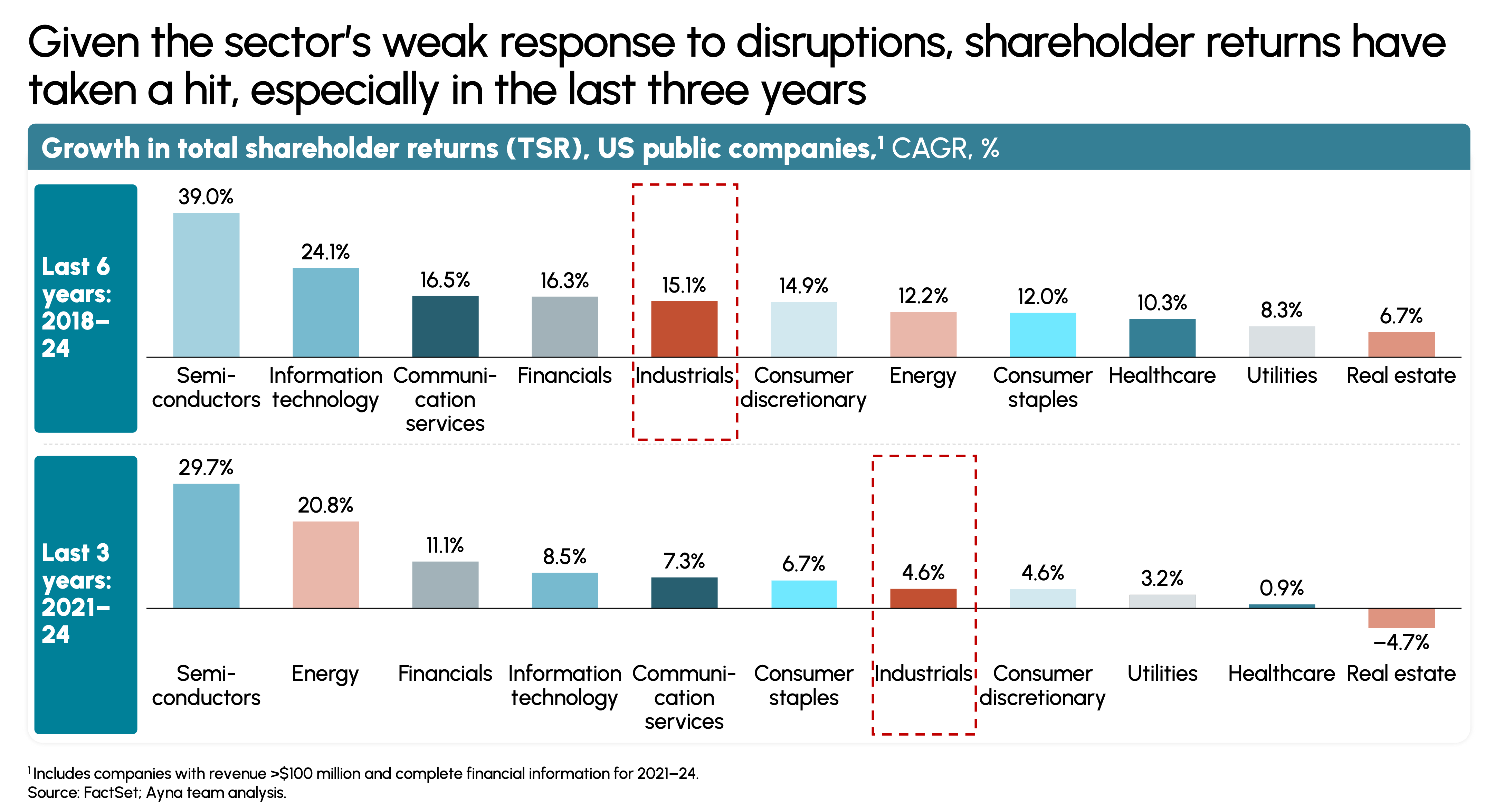

Most laggards share familiar patterns: overreliance on price hikes to offset tariffs, limited AI adoption, and lagging productivity. While other sectors are beginning to benefit from AI, industrials are seeing slower gains as legacy systems, weak data foundations, and complex operating environments constrain impact. As a result, sector TSR has eroded (Exhibit 5).

Exhibit 5

8 Core Beliefs for Value Creation

Throughout these times, numerous leaders separated themselves from the rest of the pack. From an analysis of their performance paired with findings about the new macro backdrop, eight core beliefs emerged.

- Growth is not optional: Firms that pursue growth aggressively during tough times compound revenue growth, whereas laggards never catch up.

- Where you play outweighs how you play: Strong opportunities come from secular tailwinds. The fastest growing microverticals had an average TSR growth of 7.8% from 2021 to 2024, compared to 2.7% for other microverticals.

- Tariffs are here to stay: Price hikes alone will no longer save firms. While uncertainty may reduce over time, there has been consistent tariff pressure for the past two decades. This means structural moves trump short term fixes.

- Execution is King: Successful companies excel at widening margins and managing cash conversion cycles. Firms that normalized inventory by 10 days alone lifted their operating cash flow by 100 basis points relative to peers, showing that cash is king.

- Noncore Dead Weight Is Heavier Now: The age of the industrial conglomerate is over. Laggards are penalized even more harshly when they are diversified – bottom quartile revenue growth firms delivered 4.2% TSR growth compared to 10.2% TSR growth from pure-play, vertically focused industrial firms over the past two years.

- AI is a Productivity Enabler, Not a Silver Bullet: Manufacturing sees minimal impact from AI compared to other sectors, with only time savings of 0.8% of hours worked in a week. The truth is that industrials have numerous constraints that other sectors don’t have, including poor data quality, legacy systems, complex operating models, and a talent gap. AI can accelerate gains, but ROI needs to be appropriately justified. True productivity still comes from a strong operational foundation that is augmented by AI, not substituted.

- Talent Gaps Will be Values Gaps: Investing in your talent pays dividends across the board. Companies that offered more than 20 hours of leadership training per manager delivered higher revenue per employee, gross margins, and ROIC.

- Investor Quality Defines Your Multiple: Even for small-cap industrial companies, the top valued firms have twice the level of blue-chip ownership than the bottom quartile. This is because analyst coverage matters as it signals credibility, transparency, and momentum.

A Playbook for Industrials

Grounded in the eight core beliefs, we outline a playbook industrial leaders can use to create resilience, unlock growth, and outperform peers.

Align with Growth Vectors

Pursue secular demand engines—data centers, EVs, grid modernization, and public infrastructure—and reallocate capital and leadership attention accordingly.

Tariff-Proof the Business

Build adaptive pricing engines, localize supply chains, enforce contracts, and improve pricing discipline to structurally reduce tariff exposure.

Execute Relentlessly, Augmented by AI

Strengthen fundamentals—yield, uptime, mix, footprint—and apply AI to accelerate operational disciplines, not replace them.

Sharpen the Portfolio

Become a micro-vertical leader. Consider divesting noncore businesses to simplify operations and lift valuations.

Invest in Stakeholder Capital

Build leadership depth, close talent gaps, strengthen investor engagement, and craft a compelling narrative to attract premium multiples.

Industrials face a turbulent macroenvironment, yet the path forward is clearer than it appears. Companies that internalize these beliefs—and execute against this new playbook—can achieve escape velocity and lead the next chapter of industrial value creation.